The Ultimate Business Banking Tool Kit: Your Guide to Starting, Expanding, and Managing a Business in Massachusetts

This Guide Contains:

- What is Business Banking?

- Business Banking Needs When You Are Starting a Business

- Business Banking Needs When Expanding a Business

- Business Banking Solutions to Manage Your Business Finances

- Business Finance Tips for Business Owners

- Benefits of Community Bank for Businesses

Business Banking remains a cornerstone of the U.S. economy, providing business owners access to loan products and essential financial services needed to start, expand, and manage their businesses. The total value of commercial banking loans grew by $1.5 trillion from 2021 to 2022, totaling more than $17.3 trillion. Those staggering numbers indicate that business owners can access game-changing opportunities to realize and implement their entrepreneurial vision. This business banking toolkit provides critical insights into loan products, deposit services, and growth strategies designed to help businesses succeed.

What is Business Banking?

Also referred to as “corporate banking” or “commercial banking,” this niche involves financial institutions providing services and financing options to companies of all sizes. These services and solutions are specifically designed to meet unique business challenges.

Business banking options offered by financial institutions are geared to help existing businesses grow and expand. Aside from business checking and savings accounts, business banks provide cash management solutions and lending options designed specifically for businesses.

It’s important to note that although business banking continues to grow, year over year, according to the Federal Deposit Insurance Corporation (FDIC), the number of institutions has been in steady retreat since 2002. In 2021, there were reportedly 4,236 FDIC-insured commercial banking sources, a decline of more than 140 from 2020. Much of the shrinkage is due to mergers and acquisitions, leaving fewer options for local entrepreneurs and business professionals. Fortunately, reliable local community bankers can fill this void.

How Does Business Banking Impact Your Business Finances?

The importance of separating personal and business assets cannot be understated. Some startups may initially blur the business-personal lines to power through short-term goals. Co-mingling revenue across this space creates unnecessary personal liability risk, as well as increased expenses. Reaching into personal accounts can negatively impact owners and organizations. Below are some of the risks associated with doing so.

Liability Issues

Legal professionals speak to mixing business and personal resources in terms of liability. As a new company, the leadership team likely selected business liability insurance to protect against lawsuits. Commercial insurance prevents things like a slip-and-fall accident from costing the organization tens, if not hundreds, of thousands in losses.When a business entity reaches into individual checking, savings, or credit card accounts or uses personal assets to support the company, the line between what constitutes corporate and the owners’ interests grow thin. In the event of a civil lawsuit, a complainant could successfully argue that owners and investors are personally liable in the absence of a clear separation. Once the line has been crossed, lawyers could go after your home.

Increased Risk of Getting Audited

The ranks of the Internal Revenue Service are growing, and agents will likely conduct more business audits in the coming years. Should your organization get randomly selected, auditors usually see the mixing of money as a red flag. They may decide to add another layer of scrutiny to vetting the company’s finances. On the other hand, a motivated IRS agent may see the commingling of funds as a reason to open a personal-side audit. The time, expenses, and stress involved in a two-pronged audit are not worth the risk.

Lose Business Deductions

Expenses must be supported with documentation to justify a deduction to the IRS. These typically involve sources such as business credit cards, business savings accounts, business checking accounts, and even petty cash that must trace their roots to a company transaction. Without a direct link to the business, entrepreneurs lose deductions that could otherwise improve their company’s financial position.

Benefits of Separating Business Banking Resources

Aside from the risks of not having separate business and personal bank accounts, consider the benefits below.

Accounting Efficiency

Diligently separating personal and business banking streamlines the tax preparation process and secures the deductions to which your organization is entitled. Professionals may save a few dollars when hiring a certified public accountant (CPA.)

Business Performance

The benefits of monitoring your business cash flow are invaluable. It's much easier to measure and track your business's performance when you separate your business and personal accounts.

Business Credit History

Lenders will want to look at both your personal and business credit history. Maintaining separate business and personal accounts will help your business establish its creditworthiness.

Company Credibility

The old saying that you cannot make a first impression twice exists in the business world. When building new professional relationships, the image conveyed when a personal credit card or non-commercial check is used can send the wrong message. Savvy business leaders maintain the corporate veil, a sign of professionalism, and having all your business banking ducks in a row sends a subtle, positive message.

For more reasons why it is important to keep your finances separate, review our blog "Business Finance: Why Business and Personal Accounts Should Be Separate."

Business Banking Needs When You Are Starting a Business

Starting a business ranks among the most rewarding experiences in a person’s life. Having uncovered an underserved industry niche, created a new product, or found a way to provide cheaper and better service makes you a thought leader. But 20% of startups fail within 24 months, and 45% falter before crossing the five-year threshold, according to the Bureau of Labor Statistics. Although this statistic shouldn't stop you from pursuing your dream of owning your own business, you should spend some time researching why most companies tend to fail.

Several of the notable reasons are financially motivated. Potential issues include low sales periods that strain resources, lack of business credit, pivoting to another venture, or selling to head into retirement. Those conditions do not have to impact your organization. With strong business banking support, business leaders can access the resources necessary for long-term success.

How to Start a Business in Massachusetts

Knowing how to start a business in Massachusetts tasks entrepreneurs and investors with conducting much of the same diligence needed in any state. Although nuances and resource availability differ from state to state, the following checklist can be helpful when deciding whether it is a good idea to start your own business.

Make Fact-Based Business Decisions

One of the more common failings stems from people incorporating their passion and believing others will become just as enthusiastic. Belief in a product or service is half the equation. Conducting market analysis to identify a reliable customer base is crucial. Determining whether a following will invest enough of their hard-earned money into your venture remains a key driver. If you plan to build it, be reasonably sure they will come.

Consider the Competition

Bringing a better or unique product or service to the market than competitors is a good jumping-off point. But the pie is only so large, and others in the sector are unlikely to fork over their slice.

Consider how marketing your improvement can benefit customers from a cost-effective standpoint. From this perch, you can gather that consumers select products based on value. Value is how much something costs versus the usage or enjoyment the consumer derives. Run the numbers on how your operation would initially outpace others. Then work through how competitors would react in terms of price slashing and value-added promotions.

Create a Business Plan

With the hard numbers in hand and a vision of the organization in mind, start creating your business plan. Include a mission statement, goals, company description, marketing plan, organization structure, taxes, and business banking strategies to start, grow, and expand your business. This document should help guide your business efforts for 3 to 5 years.

Build a Sound Financial Plan

Few new businesses achieve the vision entrepreneurs anticipated without seed money, credit, and an ongoing revenue stream. It's generally wise to develop a financial plan that involves the first five years. The five-year threshold often proves persuasive in attracting investors and securing business banking and financing opportunities to help you achieve your vision.

Determine What Business Type Is Best

Which type of business structure is right for your company will depend on your company's long-term goals, whether partners are involved, how much legal risk you are willing to take, and whether you'll need to hire employees. While some small businesses may operate safely as sole proprietorships, all should consider registering their company.

Sole Proprietorship is the simplest business structure owned by one person or a married couple. Unless the owner registers as an LLC or corporation, it is considered a single-owner company. In Massachusetts, sole proprietors pay personal income taxes on business profits.

Limited Liability Company (LLC) is a legal structure used to protect personal assets (home, car, bank account) in the event your business is sued. An LLC is an unincorporated association that provides limited liability to its owners (members). Generally speaking, in the absence of personal negligence, members of an LLC are not personally liable for debts, obligations, and liabilities.

Partnerships are formed when two or more individuals or organizations decide to go into business together. A partnership is not directly subject to income tax. Instead, each partner is taxed on their share of the partnership income, whether distributed or not.

Not-For-Profit organizations operate as charitable organizations and are exempt from paying taxes on the money they earn or is donated to them.

Corporation is a company or group of people authorized to act as a single entity (legally a person) and recognized as such in law. For tax purposes, there are two types of corporations: C corporations and S corporations. All corporations start as C corporations, but some can choose to be taxed as S corporations by filing a form with the Internal Revenue Service. S corporations don't pay corporate income tax. Instead, the corporation's profits pass through to the shareholder's tax returns, and each shareholder pays personal income tax on their portion. Restrictions on the type and number of shareholders apply to S corporations.

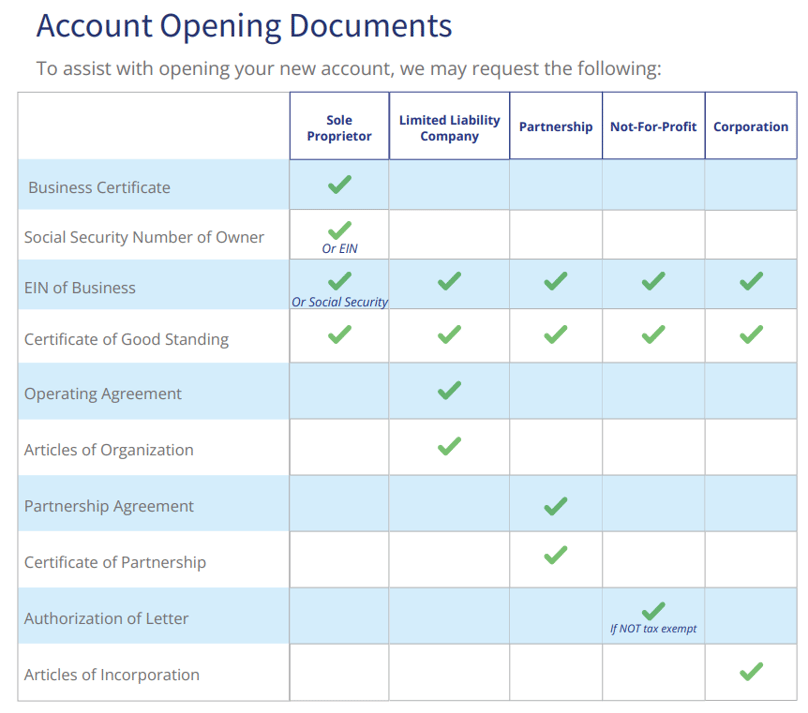

The type of business structure established will determine the documents and information you'll need to open a new business banking checking account. Some of the account opening documents listed below may not be familiar if you're a new business or considering opening a new business, so we have included a reference chart and a brief definition and explanation of purpose for each.

SSN or EIN: A Social Security Number (SSN) identifies a person, whereas an Employer Identification Number (EIN) identifies a business.

Certificate of Good Standing: A state-issued document that shows you're authorized to do business in that state and proves that you're up to date on state fees, taxes, business filings, and more. This document can be obtained from the state in which the business is registered.

Operating Agreement: It is a legal document used by Limited Liability Companies (LLC). This document outlines how the company is managed, who has ownership, and how it is structured. If more than one person is involved in the ownership of the LLC, the Operating Agreement serves as the contract between the different members.

Articles of Organization: Also called a certificate of formation. It is a document that establishes an LLC's existence and includes the business's primary details.

Partnership Agreement: This Agreement is an internal business document that serves as a contract for the partners of a company. It outlines the specific business practices, including the roles and responsibilities of each partner, details on new partners joining the company, and a variety of partner ownership and other issues.

Certificate of Partnership: A legal document filed with the state when forming a Partnership. In Massachusetts, a Limited Partnership Certificate can be completed and submitted online. A Limited Liability Partnership (LLP), not to be confused with LLC, limits the personal liability of a partner for debts, obligations, and liabilities. However, it does not eliminate liability for personal negligence.

Authorization of Letter: A legal document or letter that authorizes a third party to act on behalf of the person writing the letter.

Articles of Incorporation: A set of formal documents required by any business that wants to become a corporation or legal entity owned by shareholders and operated by a board of directors. The most popular are C corporations and S corporations. Filing requirements vary by state. In Massachusetts, a business can file online, by fax, mail, or walk-in.

Authorization of Incorporation: Formal documents filed with the state to create a corporation. Articles of incorporation generally contain pertinent information such as the firm's name, street address, agent for service of process, and the amount and type of stock to be issued.

To better understand the steps required to open a new business, review our blog "How to Start a Business in Massachusetts."

What Help is Available in Massachusetts for Small Business Owners

The Commonwealth of Massachusetts provides the following resources to people interested in starting a new business.

-

Counseling: The Massachusetts Small Business Development Center Network provides confidential, one-on-one business assistance at no cost. The Network also offers free or low-cost training programs.

-

Mentoring: Mentorship can be established through SCORE to help new business owners navigate the successes and challenges of building an organization. A nonprofit organization and SBA partner, SCORE provides a nationwide network of volunteers and expert business mentors to help small businesses get off the ground, grow, and achieve their goals.

-

Permits: The Massachusetts Permit Regulatory Office was established specifically to help new enterprises negotiate a seemingly complicated bureaucracy. Entrepreneurs can call with any permitting questions, reducing the amount of research needed to incorporate and roll out the entity.

-

Requirements: The Small Business Administration offers an online business guide that lists the requirements to start, grow, and expand your business in Massachusetts.

What Business Banking Options Are Available for New Businesses?

Lack of preparedness and business banking support prevents many startup businesses from reaching the one- and five-year marks. But 35% of organizations last almost a decade, and another 25% thrive after 15 years. Shepherding your entrepreneurial vision into a robust future calls for reliable business banking solutions like those listed below.

Business Deposit Solutions

FDIC Insurance - Deposits insured by the FDIC up to $250,000

Commercial and Small Business Lending

Experienced Lenders. Local Decision Making.

We’ll work with you to develop the best financial solution for your business.

Cash Management Solutions

Business Checking Account

Consider researching and opening a free business checking account. Some of the best financial institutions market these money-saving products as a standard option. Research what requirements are connected to your prospective business checking account. Consider the amount to open, minimum balance and monthly fee requirements, monthly transaction limitations, and check writing restrictions. If you find the right account, the restrictions will be minimal so that you can focus on your business, not your bank account.

Not all financial institutions are equal. At Middlesex Federal, we prioritize supporting our local businesses and offer a free business checking account option. Click here to learn more.

For guidance on what to compare when shopping for your business checking account, review our blog "5 Tips to Find the Right Business Checking Account For Your Business."

Business Savings Account

A business savings account provides newly orchestrated endeavors a cushion when revenue streams ebb and flow. Getting past the first year is difficult because it’s a dry run, and no one can anticipate the unknown. Consider starting a business savings account and deferring a percent of the monthly or quarterly income into the savings account.

Business Merchant Services

Working with a local bank that provides business merchant services helps simplify transactions. Credit card payments require processing and a place where owners and managers can readily access the funds. Establishing a business banking account to hold credit card payments after they are confirmed and processed streamlines access.

For a closer look at the benefits of merchant services, review our blog "5 Ways Merchant Services Can Help Your Business."

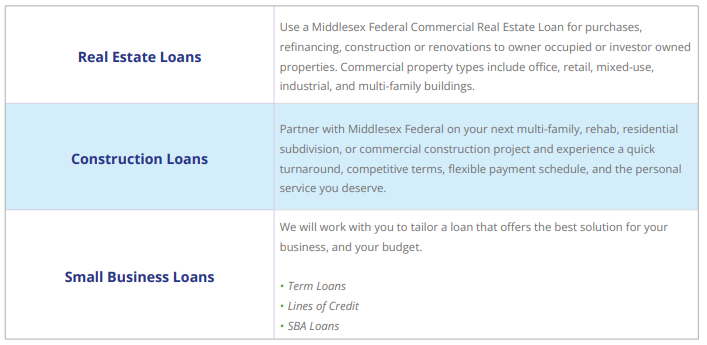

SBA Loans

The Small Business Administration backs loans for startup organizations that qualify. This loan product can be used for working capital, refinance debt, or purchase necessary equipment and materials, among other uses. SBA loans provide low-interest rates to those who meet the FICO score and financial criteria. These fixed-rate loans are usually paid in monthly installments. However, variable-rate SBA loans may also be an option.

Other Loans

An SBA loan is not a one-size-fits-all solution; business owners may be best served by considering other options. Construction loans remain a niche borrowing opportunity that accounts for the nuances of developments, expansions, renovations, and other buildouts. Commercial real estate loans open doors that allow business owners to finance the purchase or renovation of a commercial property.

It is essential to understand that entrepreneurs do not necessarily have to start a company or maintain a company on a shoestring budget and struggle with underfunding issues. There are wide-reaching financial support systems available in the Commonwealth.

Business Banking Needs When Expanding a Business

Growing organizations that want to capitalize on their success must have the resources to pull off an expansion without negatively affecting the status quo. Several business banking resources can be leveraged to further expansion goals without upsetting the delicate balance of company success.

Decision-makers who establish a business savings account may have accumulated the funds to use. However, it's generally a good idea to maintain the business savings account because it also serves as a resource in emergencies.

Coupling a portion of your savings with a business loan can also deliver the upfront funds needed to grow. If your projections are accurate, an SBA loan, construction loan, or commercial real estate loan could be a tool to help achieve expansion.

Questions to Ask When Considering a Business Expansion

Before expanding your business, consider conducting research and taking the time to establish a plan. These two steps can help ensure a successful venture. The questions below can help you get started.

Why do you want to expand a viable operation?What do you stand to gain from an expansion?

What are the risks of investing in business growth?

What are your short- and long-term goals?

When is the best time to expand the organization?

What resources do you have to fund your expansion?

Can you maintain high-level services during an expansion?

Checking to ensure you have the staffing and customer support to increase your market share is also important.

What Business Banking Options Are Available When Expanding a Business?

It's not uncommon to have attractive products, services, and a thriving business without the resources needed to expand. Forward-looking business leaders find this position among the most frustrating imaginable.

But there are business banking solutions for those with an enterprise headed in the right direction. An increased number of growing small and mid-sized companies are finding that local lending institutions offer flexible funding options with competitive rates and favorable terms. These are the most popular solutions when expanding an operation.

Business Line of Credit

One of the primary reasons to secure a business line of credit involves short-term funding. An enterprise generally sets up a line of credit to pull money out of to finance things like new equipment, renovations, supplies, and the infrastructure surrounding an expansion.

For guidance on the best ways to use a business line of credit to grow your business, review our blog "6 Ways a Business Line of Credit Can Help You Expand Your Business."

Business Term Loans

A business term loan is another product designed to provide increased expansion flexibility. Borrowers generally need reasonably sound credit to qualify for this lump sum loan.

Business term loans often include no penalty for early repayment. But the big perk for growing organizations involves flexible terms. This class of business loan can involve a schedule of a few months to 10 years in some cases.

Real Estate Loans

Also called a "commercial real estate loan" or CRE, this is a secured mortgage because the property serves as collateral. Income-producing properties such as office buildings, manufacturing plants, hotels, and retail outlets, among others, are natural fits for using real estate loans.

Down payments usually run from 20 to 30 percent of the commercial building's purchase price. Interest rates tend to be relatively low, and some programs are backed by the SBA. Borrowers may be able to choose from variable or fixed rate options.

It's important to consult with a loan professional about the many differences between real estate loan options to ensure which solution is best for the needs of the business.

Construction Loans

These short-term loans are leveraged for the purposes of building a commercial or residential property. They typically come with higher interest rates, later replaced by a long-term mortgage option. Construction loans are popular among developers, builders, and even house flippers who plan to turn a profit on the sale or lease of a property. Approvals require a sound business plan, construction timeline, costs, and architectural designs.

Bridge Loans

Bridge loans usually run from six months to three years and are considered a short-term funding option. Business leaders sometimes choose these loan products to take advantage of opportunities while waiting for long-term financing.

Business Banking Solutions to Manage Your Business Finances

When business leaders become distracted and bogged down with day-to-day minutia, it can prevent a business from succeeding. Work with a local bank that offers cash management services that complement your business accounts and help you manage your business finances efficiently.

Below is a list of cash management tools and services available to business owners.

Online & Mobile Banking

You or an authorized user can manage your business accounts from a phone, PC, or tablet.

- Pay a person or a bill.

- Check your balance.

- Stop a payment.

- Transfer funds between accounts or bank to bank.

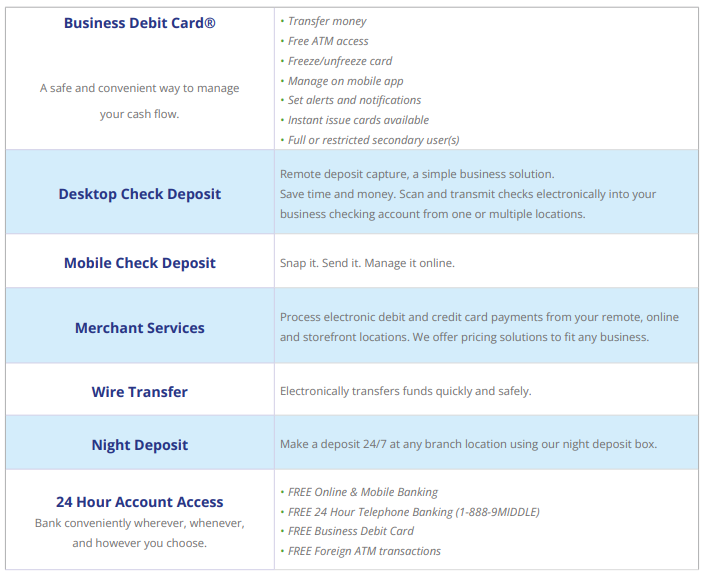

Mobile and Check Deposit

Remotely deposit checks directly into your business checking or savings account from your phone or desktop. Within your mobile app, you snap a picture of your check, verify and submit it. Desktop Remote Deposit Capture lets you scan and transmit checks electronically from one or multiple locations. Both options offer a simple business solution that saves time and money.

Business Debit Card

Let's you monitor and control card activity from your phone and comes with security chip protection. It offers a safe and convenient way to manage your cash flow.

Merchant Services

The primary decision-maker of an organization should not be concerned about the routine processing of credit card payments. A reliable merchant services program can see the electronic payment system through to your business account. Electronic debit and credit card payments are processed from your remote, online, and storefront locations.

We offer pricing solutions to fit any business. A reliable merchant services resource

Find out how you can stream line customer payments, review our blog 5 Ways Merchant Services Can Help Your Business.

Business Payroll Services

Weekly payroll has become something of a chore, and changing government regulations only adds to the problem. Outsourcing payroll services to a third party remains a cost-effective option that alleviates the need for an internal hire.

Business Fraud Protection

While working with your business finances, it is crucial to keep your data safe. Everything from your bank account information to computer systems and physical buildings can potentially expose sensitive information. In addition to adding security measures to your technology and physical structures, be sure to have your employees participate in regular training to reduce potential opportunities for error. Fraud protection services are also available within some online banking platforms; they monitor transactions and provide alerts when something appears unusual. These may include check-monitoring, and ACH intervention which can be set and managed according to the levels of restrictions business owners would like in place.

To learn how you can protect your business against fraud and identity theft, review our blog 6 Ways to Protect Against Business Fraud and Identity Theft."

Business Finance Tips for Business Owners

Small and mid-sized businesses are often successful because of their leadership, vision, hard work, and unique skill sets. These business finance tips are worth considering if you are ready to start your own business.

Create a budget, and stick with it.Pay yourself a salary.

Save money for growth.

Develop an efficient billing method.

Know what business loans can help you succeed.

Maintain good business credit.

Stay on top of quarterly tax payments.

Periodically review expenses.

Remain open to competitive vendor bids.

Invest in qualified personnel and data security if applicable.

Keep your personal and business finances separate.

Seek guidance from professionals.

Cash Flow Tips

How a business venture handles its day-to-day cash flow significantly impacts the big picture. Incoming revenue may involve seasonal peaks and valleys, making business banking strategies increasingly important. These are cash flow tips worth considering.

Collect receivables as quickly as possible.Strategically pay bills.

Set up a business line of credit.

Negotiate with suppliers on an ongoing basis.

Select a suitable payroll cycle.

Manage credit responsibly.

Use a business debit or credit card for transactions.

For more cash flow tips, review our blog "7 Cash Flow Management Ideas for Small Businesses."

Benefits of a Community Bank for Businesses

As a local business owner, you understand the importance of supporting local businesses. Local community banks match your desire to improve the local economy and offer services to local businesses to help the community and its members thrive. Completing your business banking transactions and solving your lending needs with local solutions can provide several advantages for business owners.

To a local community bank, your business means an opportunity to build a relationship and help you and the community succeed. Local insight into the surrounding market offers a better chance at loan approval than a large financial institution unaware of local economic shifts. When you need financing fast, a local community bank can provide faster decisions and approvals. They set their own guidance and timelines. Unlike larger financial institutions, local banks don't need to wait for a decision from corporate headquarters, which could be located across the country.

In addition, business owners enjoy the added benefit of developing a strong relationship with their community banker.

How Middlesex Federal Can Help Start, Expand, and Manage Your Business

If you are ready to start or expand a business, Middlesex Federal Savings' business banking solutions can help you manage and grow your operation. Contact us today to discuss how our business deposit and lending solutions can help your business succeed.